Did Galeterone ARMOR2 Prostate Cancer Data Impress at ESMO 2014?

At the 2014 ESMO Congress in Madrid, Mary-Ellen Taplin, MD (Dana-Farber Cancer Institute, Boston) presented the results of the Tokai Pharmaceuticals (NASDAQ $TKAI) ARMOR2 clinical trial of galeterone in men with advanced prostate cancer.

Galeterone has a novel triple mechanism of action. In effect, it is a CYP17 lyase inhibitor (like abiraterone) that has additional anti-prostate cancer actions including androgen receptor (AR) inhibition (like enzalutamide). It also causes AR degradation that decreases AR levels.

Tokai’s IPO last month is reported by Renaissance Capital to have raised $98M for the company, with most of the funds going to prior investors including Novartis Bioventures which owned 28 percent.

Shares in $TKAI were initially priced at $15. They soared to a high of $30 thanks to high insider buying and a high trading volume. Novartis Bioventures were reported by Renaissance to have bought $20M.

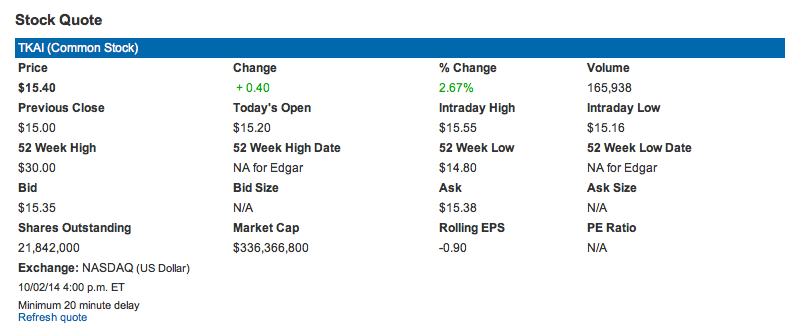

As of publishing this post, the stock is now trading at $15.40, slightly above it’s IPO price. So have Novartis and others made a good investment?

The market cap of $TKAI, according to their Investor Relations page (screenshot pre-market Oct 3, 2014 shown above) is $336M – not high for a company about to enter phase III drug development.

The market cap of $TKAI, according to their Investor Relations page (screenshot pre-market Oct 3, 2014 shown above) is $336M – not high for a company about to enter phase III drug development.

Readers are no doubt aware of the Feuerstein-Ratain rule that predicts a phase III cancer trial will be a failure when undertaken by a company with a market cap less than $300M. As Adam noted in his May 6 story on The Street earlier this year, “For companies with market caps between $300 million and $1 billion, the oncology phase III success rate is 59%.”

The big questions now are did the data for galeterone from the ARMOR2 trial impress at ESMO 2014 in Madrid and what are the challenges and opportunities in the planned phase III ARMOR3-SV trial?

Subscribers can login to read more.

DISCLAIMER: Please note this piece offers no stock advice, is not a solicitation to invest in $TKAI and makes no recommendation on whether to buy or sell. It merely offers commentary and analysis of the data presented at ESMO 2014. Readers should do their own due diligence prior to making any investment decision.

This content is restricted to subscribers

2 Responses to “Did Galeterone ARMOR2 Prostate Cancer Data Impress at ESMO 2014?”

Thanks Pieter, great post, lots of facts I did not know about.

It did occur odd to me that ARV7 patients should be resistant to a CYP17 inhibitor. One explanation for this is intratumoral upregulation of CYP17. If you’re a believer, then at ESMO Gal degrades the excess of androgen produced by upregulated CYP17 that Abi is unable to block in NEJM. The only solace to this yet another leap of faith is that in ARMOR3 Gal is going against an AR blocker.

Another good question that was posed is why do ARV7 patients respond to Gal initially but not after Abi/ Enza? Perhaps in addition to developing ARV7 variant, clonal evolution of other onogenic pathways, like PI3K-AKT, is also taking place. After all, hormone resistance is a concept that was widely embraced in the pre-Abi/ Enza era.

Thanks Maxim for your considered comments, glad you liked the piece. I agree with you that other oncogenic pathways such as PI3K may be at play in patients with acquired resistance. ARMOR3 does seem to be a leap of faith, but the results will be informative either way.

Comments are closed.